Imagine yourself driving on the bustling streets of your city or town, the lights illuminating the skyline as you navigate through the traffic with precision. Suddenly, a distracted driver comes into your path, resulting in a nerve-wracking collision! An unexpected twist to the story, is it not? Amidst the chaos and frustration, one thought echoes in your mind - insurance. Point being - despite being a cautious and skilled driver, accidents happen, and they can be downright stressful. In moments like these, having the right car insurance makes all the difference! It comes in to save the day, providing financial protection when you need it most. However, when you buy insurance, it is just the first step, navigating the process of claiming car insurance for your own damage demands careful attention to detail. From assessing the scene of the incident to coordinating with your insurance provider, each step is crucial in ensuring a smooth journey towards resolution.

But first, let’s look at what an own-damage car insurance claim is.

What is an Own Damage Car Insurance Claim?

An own damage car insurance claim is your lifeline when unexpected mishaps happen involving your beloved vehicle. Under a comprehensive policy or standalone own damage coverage, this type of claim allows you to seek compensation for damages incurred by your car due to accidents, fire, theft, and other covered perils.

However, the road to recovery begins with swift action. Once the incident occurs, it's imperative to notify your insurer promptly and gather all necessary documentation to kickstart the claim process. Your insurer will then dispatch a surveyor to assess the extent of the damages firsthand.

Once the surveyor's report is in hand, you can proceed to file your claim for reimbursement of repair or replacement costs. But here's where it gets interesting – you have the control to choose between two paths: the 'cashless claim settlement' or the 'reimbursement claim.'

Think of it as choosing between two different routes to your destination: one offers convenience and efficiency, while the other provides flexibility and control. Let's explore these options further to ensure your journey to claim settlement is as smooth as can be.

Types of Claim Settlements

Let's look at the two types of claim settlements -cashless claim and reimbursement claim, in detail.

-

Cashless Claim

Imagine your car needs fixing, and you take it to a garage approved by your insurance company. This kicks off a cashless claim settlement process. Just as the name suggests, everything happens without cash changing hands. You won't need to pay any money to the insurer's authorised garage for the repair work. Instead, the insurer directly pays the garage for the repairs, covering the claim amount. The only costs you might have to cover are the compulsory deductible and any voluntary deductible you opted for when you purchased the policy. - Reimbursement Claim

Now, let's say you decide to get your car repaired at a garage outside the insurer's authorised network. This triggers a reimbursement claim settlement process. Here's how it works: You foot the bill for the repairs at your chosen garage, and later, you can claim the repair costs back from your insurer. After reviewing your claim, the insurer reimburses you the entire claim amount, taking into account any applicable deductibles—compulsory and voluntary, if you chose one.

Your Rights Under IRDAI — Claim Settlement Timeline

Under IRDAI Motor Insurance guidelines, your insurer is legally required to settle your valid claim within 30 days of receiving all documents. For cases requiring investigation, this extends to 45 days.

If your claim is delayed beyond this without a valid reason, file a grievance at IRDAI's IGMS portal (igms.irda.gov.in) or call Bima Bharosa (1800-103-1961).

Documents Required To Claim Car Insurance

In the car insurance claims process, having the right documents is crucial. Here's a detailed checklist -

- Completed Claim Form: Fill out and sign accurately.

- Insurance Policy Copy: Confirm your coverage.

- Tax Payment Receipt: Provide proof of tax payment.

- Repair Cost Estimate: Get a signed estimate from the repairer.

- Original Repair Invoice: For cashless claims, only the invoice is needed.

- Claims Discharge Cum Satisfaction Voucher: Sign across a revenue stamp.

- Driver's License Copy: Provide a verified photocopy.

- Registration Certificate Copy: Include a verified photocopy.

- Proof of PAN (Pan Card): Provide proof of your PAN.

- Proof of Aadhar (Aadhar Card): Provide proof of your Aadhar.

- Pollution Under Control Certificate Copy: Include a photocopy.

- Cancelled Cheque/Passbook: For reimbursement claims.

Remember, requirements may vary by insurer. Always double-check for a smooth claims process.

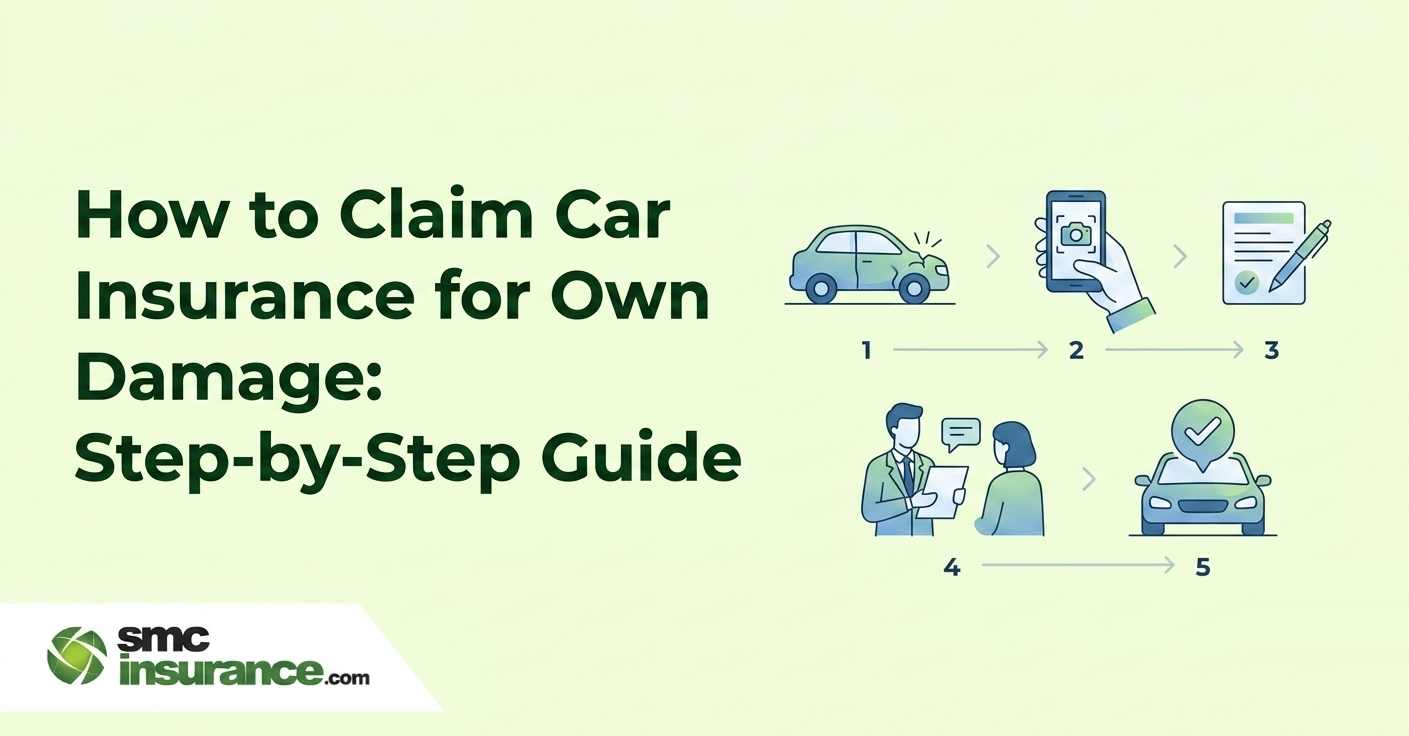

Learn How to Claim Car Insurance For Own Damage? Step-by-Sep Process

Wondering about the steps for claiming car insurance for own damage? Do not worry, as the process is methodical and straightforward. After experiencing an accident, initiating a claim with your car insurance provider requires a comprehensive understanding of the procedure. Here's a breakdown of the steps to claim insurance for car damage:

Step 1: Inform Your Insurance Provider

Reach out to your insurance company immediately to report the incident and provide detailed information

about the damages to your vehicle. Transparency is crucial to avoid complications during the claims process.

Step 2: File an FIR with the Police

If the situation demands, file a First Information Report (FIR)

with the police as soon as possible after the accident. This is necessary in cases of theft, car accidents, or fires. However, minor scratches and dents may not require an FIR unless a third party is involved.

Step 3: Gather Photographic Evidence

Capture as many clear and discernible photos as possible

of the accident scene and the damage to your vehicle. These visuals are instrumental in enabling your own damage insurance provider to assess the extent of the damages accurately.

Step 4: Provide Required Documentation To Your Insurance Company

Ensure you furnish your insurance company with all the necessary paperwork to

facilitate the claim process. This includes a copy of your insurance policy, the FIR (if applicable), your driver's licence, and

the car registration certificate.

Step 5: Arrange Repairs For Your Vehicle

Once your claim is approved, you can proceed with getting

your vehicle repaired at a workshop of your choice. However, it's crucial to wait for approval from the surveyor before

initiating any repair work.

Step 6: Navigate The Claim Settlement Process

If you go for the cashless claim settlement option,

the repair expenses are directly deposited with the network garage upon receipt of the surveyor's final report.

Alternatively, for reimbursement settlement claims, you need to provide your insurance company with the repair amount receipts.

It's essential to note that while your own damage insurance provider will contribute a necessary portion to the cost of repairing your vehicle, you are still responsible for paying the mandatory deductible.

Important Factors to Remember When Making Claims for Own Damage Car Insurance

Here are some key points to remember when raising own damage car insurance claims -

- Prompt Notification: Notify your insurance provider immediately after the incident, preferably within 24 hours. Delayed notification may result in claim denial.

- Police Involvement: If necessary, report the incident to the police and ensure that a First Information Report (FIR) is filed at the nearest police station as required.

- Assess the Situation: Evaluate the extent of damage and choose the appropriate course of action. For minor damages, consider utilising the No Claim Bonus (NCB) instead of filing a claim.

- Accurate Information: Ensure that all information provided on the claim form is accurate and truthful. False information can jeopardise your claim.

- Legal Compliance: Adhere to legal requirements and follow the prescribed processes in case of an accident. Gather all necessary documents to support your claim.

- Dispute Resolution: Refrain from immediately agreeing to a resolution with the third party involved in the incident. Avoid engaging in conflicts and eventually strive to reach a mutually agreeable resolution to minimise misunderstandings.

By keeping these points in mind and following the proper procedures, you can streamline the process of raising own damage car insurance claims and increase the likelihood of a successful outcome.

Top Reasons Own Damage Claims Get Rejected

Here are some of the reasons why your claim can get rejected:

- Delayed intimation (beyond 24-72 hours after incident)

- Driving under the influence of alcohol or drugs

- Driving without a valid license

- Policy not active at the time of damage

- Damage from unauthorized vehicle modifications

- Wear and tear submitted as accident damage

- Damage from racing, trials, or off-road use (unless covered by add-on)

Digital Claim Filing

In 2024-25, most insurers allow digital own damage claims for minor damages. Via your insurer's app or website, you can:

- Register the claim online.

- Upload photos/videos of the damage.

- Get digital survey approval.

- Proceed to the network garage for cashless repair.

No waiting for a physical surveyor for minor claims.

Summing Up!

In conclusion, navigating the complexities of claiming car insurance for own damage demands meticulous attention to detail and adherence to proper procedures. Despite being a cautious driver, accidents can still occur, underscoring the importance of having the right insurance coverage. Whether opting for a cashless claim settlement for convenience or a reimbursement claim for flexibility, the process involves essential steps, from promptly notifying your insurer to providing necessary documentation and coordinating repairs. By understanding the nuances of the claims process and following key points, such as prompt notification, legal compliance, and accurate information provision, you can pave the way for a smoother journey towards resolution. Remember, in moments of uncertainty and stress, your car insurance serves as a reliable lifeline, offering financial protection when you need it most.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

FAQs

Yes, you're eligible to claim insurance for car scratches if your policy covers own damage. However, it's important to note that for minor scratches, it might be more cost-effective to pay out of pocket, considering the deductible for the claim.

Damage to the car bumper is typically covered under the Comprehensive Insurance Plan, not under the Third-party Insurance Plan.

The time limit for filing a car insurance claim post-accident varies among insurance companies. Typically, you have between 48 to 72 hours to file a claim. However, exceptions exist, as certain circumstances may prevent a claim from being filed within the stipulated time frame.

Yes, denting painting is covered by insurance.

You can claim insurance for minor damages to your car without filing an FIR. However, an FIR is required in cases involving third-party involvement, fire accidents, or theft.

You can claim insurance for minor damages to your car without filing an FIR. However, an FIR is required in cases involving third-party involvement, fire accidents, or theft.

As per IRDAI guidelines, insurers must settle a valid motor insurance claim within 30 days of receiving all required documents. If the claim requires additional investigation (e.g., fraud suspected), the deadline extends to 45 days. If your insurer delays beyond this, you can raise a complaint with IRDAI at igms.irda.gov.in.

Yes, for minor damages like dents, scratches, and broken glass where no third party is involved, an FIR is not required. However, an FIR is mandatory for:

- Theft of the vehicle,

- Fire accidents,

- Accidents involving third-party injury or property damage.

Always check with your insurer before skipping the FIR.

Common reasons include:

- Delayed intimation beyond the specified window.

- Drunk driving at the time of accident.

- Driving without a valid license.

- Policy lapsed at the time of accident.

- Damage caused by unauthorized modifications to the vehicle.

- Wear and tear presented as accident damage.

Always inform your insurer immediately and ensure all documents are accurate.

The compulsory deductible is a fixed amount you must pay out-of-pocket whenever you file a claim. For private cars: Rs. 1,000 for vehicles up to 1500cc and Rs. 2,000 for vehicles above 1500cc. For two-wheelers, it is Rs. 100. This is separate from any voluntary deductible you may have chosen to reduce your premium.

For cashless claim settlement, you must take your vehicle to a garage that is within your insurer's authorized network. Repairs at non-network garages will require you to pay upfront and then seek reimbursement. Always check your insurer's cashless garage list (most insurers have an online locator) before deciding where to go.

Yes, most major insurers now offer digital self-inspection for minor damage claims. You upload photos or a short video of the damage via the insurer's app, which triggers a digital survey. This is faster than waiting for a physical surveyor. However, for major damage or total loss cases, a physical survey is still mandatory.