Yes, bike insurance allows claims for scratches and dents under a comprehensive policy. But for repairs under Rs. 2,000–Rs. 3,000, paying out of pocket is usually cheaper than losing your No Claim Bonus and facing higher premiums. Claims are best used for significant damage.

A small scratch on the tank or a dent on the mudguard can feel bigger than it is. Not because of the damage, but because of what follows. You start thinking about repainting, costs and whether your insurance should cover it.

Most riders assume the answer is simple. You’ve paid your premium, so the insurer should fix it. But once you actually try to claim, things get complicated. Deductibles come into play. Your No Claim Bonus disappears. And suddenly, a Rs. 1,500 repair starts affecting next year’s premium.

That’s where the real question begins. Not whether you can claim, but whether you should. By the end of this guide, you’ll know exactly when using bike insurance for minor damage makes sense and when it quietly works against you.

Does Bike Insurance Cover Scratches and Dents?

Let’s start with what the policy allows. Yes, bike insurance covers scratches and dents, but only under the right type of plan.

Types of Coverage That Matter

|

Policy Type |

Covers Scratches & Dents? |

Notes |

|

No |

Only covers damage to others |

|

|

Yes |

Includes own damage cover |

A comprehensive policy includes “own damage” protection, which covers accidental damage to your bike. That sounds straightforward. But coverage depends on one key condition.

Wear and Tear vs Accident: The Fine Line in Bike Insurance

This is where most claims fail. Insurance does not cover everything that looks like damage.

What Counts as Wear and Tear?

Under guidelines followed across insurers and regulated by Insurance Regulatory and Development Authority of India, the following are excluded:

- Paint fading due to sunlight

- Scratches from regular usage

- Rusting or ageing

- Surface dullness

What Counts as Accidental Damage?

- Scratches from a fall

- Dents from collision

- Impact from external objects

What Insurers Actually Check Before Approving a Scratch Claim?

Even when damage looks valid, approval is not automatic. How Surveyors Evaluate Minor Damage

- Freshness of damage: Old scratches with rust are usually rejected

- Consistency of impact: Damage should align with a single incident

- Location of scratches: Random marks across panels raise doubts

- Photo evidence: Immediate documentation strengthens claims

Here’s what most people miss. If the insurer cannot link the damage to one clear event, the claim may not go through.

What’s Changed in Motor Insurance 2026

-

Increased standardisation of policy wordings across insurers

- Digitisation of claim processes and faster approvals

- Stronger fraud monitoring and claim verification frameworks under IRDAI

- Wider adoption of add-ons like zero depreciation and NCB protection

Should You Claim Bike Insurance for Minor Scratches?

This is where the decision shifts from technical to practical. You can claim. But in many cases, you shouldn’t.

What Happens When You File a Claim?

- You lose your No Claim Bonus (NCB)

- Your next premium increases

- You still pay a deductible

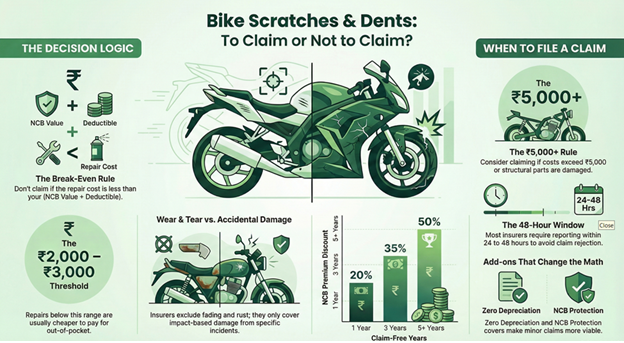

No Claim Bonus (NCB) Explained

|

Claim-Free Years |

NCB Discount |

|

1 year |

20% |

|

2 years |

25% |

|

3 years |

35% |

|

4 years |

45% |

|

5+ years |

50% |

Note: Even a small claim resets this benefit to zero. No Claim Bonus applies only to the own-damage premium component. The third-party premium is fixed by IRDAI and does not change based on claims.

The “Break-Even” Rule: How to Decide Quickly

Instead of guessing, use a simple check.

Break-even = NCB value + Deductible

Example

- NCB value: Rs. 2,000

- Deductible: Rs. 300

- Total impact: Rs. 2,300

If repair cost is below Rs. 2,300 then don’t make a claim

If above, consider making a claim

This one calculation prevents most bad decisions.

Real Cost Comparison: Claim vs Self-Pay

Numbers make the decision clearer.

|

Scenario |

Repair Cost |

NCB Loss Impact |

Total Cost |

|

Pay yourself |

Rs. 800 – Rs. 2,000 |

Rs. 0 |

Rs. 800 – Rs. 2,000 |

|

Claim insurance |

Rs. 800 – Rs. 2,000 |

Rs. 1,500 – Rs. 5,000 |

Higher overall |

Note: This is just an estimate. Costs vary by bike model, insurer and city. Figures are indicative.

Deductibles: The Cost You Still Pay

A compulsory deductible is a fixed amount that must be paid by the policyholder for every claim. It is mandated under IRDAI regulations and applies uniformly across motor insurance policies. Even with a claim, you don’t get full coverage. Most two-wheelers have Rs. 100 compulsory deductible per claim. A voluntary deductible is optional and can reduce your own-damage premium, but increases your out-of-pocket cost during claims.

Note: Exact amount may vary slightly based on insurer and policy terms.

Depreciation and Why Small Claims Pay Less

This is where expectations often break. Without add-ons, insurers deduct value based on part type.

Typical Depreciation Rates

- Plastic, rubber and nylon parts may attract depreciation of up to 50% as per standard motor insurance norms.

- Fiberglass: around 30%

- Metal parts: 5% to 50% based on age

Most scratches affect plastic panels. That means you often receive only half the cost.

Partial Repair vs Full Replacement: What Makes Sense?

When you visit a garage, you’ll usually get two options.

Local Repair

- Rs. 500 – Rs. 1,500

- Quick fix

- Slight imperfections

Full Replacement

- Rs. 2,500 – Rs. 6,000+

- Better finish

- Often required for claims

Here’s where it gets tricky. Insurance claims usually push toward full replacement, increasing the bill. If you’re paying yourself, local repair is often enough.

Garage Influence: Why You’re Often Told to Claim

This part surprises most riders. Garages often recommend insurance because:

- Replacement jobs bring higher billing

- Insurance approvals support larger repairs

- Margins are better

Before deciding, always ask for two estimates:

- Cash repair

- Insurance-based repair

The difference can be significant.

How Claim Frequency Affects Your Insurance Profile

A single claim may not hurt much. Repeated small claims do. Over a long term, it can have higher renewal premiums, stricter claim scrutiny and reduce flexibility with insurers. Over time, even frequent minor claims make your policy more expensive.

Claim Timing Matters More Than You Think

Timing can change the outcome. If your policy is about to renew:

- A claim resets your NCB immediately

- You lose accumulated discounts

So the smarter approach is if damage is minor and renewal is close, delay the claim and repair it yourself.

When It Actually Makes Sense to Claim Bike Insurance

Not all damage should be treated the same.

Make a claim if:

- Repair cost is above Rs. 5,000

- Structural parts are affected

- Multiple components are damaged

- Your NCB is low

Avoid claiming if:

- Damage is cosmetic

- Repair cost is under Rs. 2,000–Rs. 3,000

- You have high NCB

Add-ons That Can Change the Decision

Some riders make small claims more viable.

- Zero Depreciation Cover: Covers full part cost

- NCB Protection: Allows limited claims without losing NCB

- Consumables Cover: Covers oils, bolts and minor items

Even then, small claims may not always be worth it.

Cost of Buying Bike Insurance in India

Understanding cost helps put claims in perspective.

|

Bike Type |

Annual Premium |

|

100–150cc |

Rs. 1,200 – Rs. 2,500 |

|

150–350cc |

Rs. 2,000 – Rs. 5,000 |

|

Premium bikes |

Rs. 4,000 – Rs. 10,000+ |

Note: Premiums vary by city, insurer, IDV and add-ons.

A small claim today can increase your premium tomorrow. The right policy setup reduces that risk. Before you buy bike insurance or renew, compare plans that balance coverage and cost at SMC Insurance.

How to File a Bike Insurance Claim for Scratches and Dents

Once you’ve decided the damage is worth claiming, the process is fairly structured. Where most people go wrong is not the complexity, but the sequence. Missing one step or rushing repairs can lead to delays or even rejection. Let’s walk through it the right way.

- Step 1: Check If the Damage Is Worth Claiming

Not every scratch deserves a claim. Look at the damage and get a rough repair estimate from a nearby garage. If the cost is minor, it may not justify losing your No Claim Bonus. If the damage is clearly from a recent incident and repair costs are meaningful, move ahead.

- Step 2: Capture Evidence Immediately

Take a few clear photos of the damage before doing anything else. Include both close-up shots and wider angles so the insurer can understand the context. Blurry or poorly lit images often lead to unnecessary questions later. A short video can also help if the damage is spread across multiple areas.

- Step 3: Inform the Insurer Without Delay

Most insurers expect you to report the incident within 24 to 48 hours. This can be done through their app, website, or customer care number. You’ll need to share basic details such as your policy number, when the damage occurred, and a short explanation of what happened. Even if the damage looks minor, don’t delay this step. Late reporting is one of the easiest reasons for a claim to be rejected.

- Step 4: Register the Claim and Note the Reference Number

Once the insurer logs your request, a claim reference number is generated. This becomes your tracking ID for the entire process. Keep it handy. You’ll need it when speaking to the insurer or the garage.

- Step 5: Decide How You Want to Repair the Bike

At this stage, you choose between a cashless claim and a reimbursement claim. In a cashless setup, you take the bike to a network garage and the insurer settles most of the bill directly. In a reimbursement claim, you get the repair done anywhere, pay upfront, and then submit bills for repayment. For small dents and scratches, cashless is usually easier and faster.

- Step 6: Wait for the Surveyor’s Inspection

This is the step you should never rush. The insurer will assign a surveyor to inspect the damage. Depending on the insurer, this could be a physical visit or a video inspection. The surveyor’s job is to confirm that the damage matches your claim and is genuinely accidental. Do not start repairs before this inspection is completed and approved. If you do, the insurer may refuse to pay.

- Step 7: Submit Basic Documents

You’ll be asked for a few standard documents: -

- Policy copy

- Registration Certificate (RC)

- Driving licence

- Photos of the damage

For simple scratch or dent claims, an FIR is usually not required unless there’s theft or third-party involvement.

- Step 8: Review the Repair Estimate Carefully

The garage will share a repair estimate with the insurer, who then approves the payable amount after applying depreciation and deductibles. This is a crucial checkpoint. Ask the garage or insurer what your final out-of-pocket cost will be. Sometimes, even after approval, your share remains high enough to reconsider the claim.

- Step 9: Get the Repair Work Done

Once approval is in place, the garage proceeds with the repair. Depending on the extent of damage, this could involve repainting, part repair, or full replacement. Stay in touch with the garage, especially if parts need to be ordered.

- Step 10: Final Payment and Settlement

- If you choose cashless, the insurer pays the approved amount directly to the garage. You only pay your share, which includes the deductible and any depreciation.

- In a reimbursement claim, you settle the full bill first and then submit invoices to the insurer. The approved amount is credited back to you later.

Cashless vs Reimbursement: What Works Better for Small Damage

|

Feature |

Cashless |

Reimbursement |

|

Payment |

Insurer pays garage |

You pay first |

|

Speed |

Faster |

Slower |

|

Effort |

Lower |

Higher |

For minor damage, reimbursement often feels unnecessary.

How Insurers Handle Multiple Small Damages

If your bike has several scratches:

- They may be treated as separate incidents

- Multiple claims may be required

- Each claim includes a deductible

This makes claiming impractical in most cases.

Must Read Guide From SMCInsurance

- Does Bike Insurance Cover Engine Damage from Water?

- Flood Damage and Bike Insurance: Is Your Two-Wheeler Actually Protected?

- How to Transfer Bike Insurance After Sale

- Long-Term vs Annual Bike Insurance

- Is It Safe to Buy Bike Insurance Online Instead of Through an Agent?

- Will Your Insurance Pay if Your Bike is Stolen From Outside Your House

Wrapping Up,

Scratches are part of owning a bike. They feel bigger than they are, especially when the bike is new. Insurance can fix them. But it is not designed for every small imperfection. Each claim has a cost beyond the repair. Lost discounts, higher premiums and added effort.

So pause before filing. Check the repair estimate, compare it with your NCB and use the break-even rule. If the numbers don’t favour you, pay and move on. Use insurance where it matters. That’s how you keep it valuable.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

FAQs

Yes, if you have a comprehensive policy. But small claims often lead to higher long-term costs due to NCB loss.

Yes, your No Claim Bonus resets, which increases renewal premium significantly.

Typically above Rs. 2,000–Rs. 3,000. Below that, self-payment is usually cheaper.

Yes, it reduces repair costs. But it does not protect your NCB unless combined with NCB protection.

Yes, but frequent claims increase premiums and scrutiny.

No, it does not cover your bike’s damage. You need comprehensive coverage.

Only if your bike is new or expensive. Choose add-ons based on usage and risk.