Bharat Griha Raksha is IRDAI's standard home insurance policy, mandatory for every general insurer to offer since April 2021, covering the home building, home contents, or both against fire and allied perils including natural calamities, riots, strikes, malicious damage, terrorism and other insured events under a standard IRDAI-prescribed policy wording. Basic structure cover can start as low as Rs. 250 a year for smaller sum insured amounts, while comprehensive structure-plus-contents cover for a mid-value home typically runs Rs. 2,000 to Rs. 10,000 annually. Since the policy wording is fixed by regulation, your main decision is choosing the right sum insured and comparing insurers on price, add-ons, and claim service rather than coverage terms.

A pipe bursts at 2 AM and floods your living room. Or a cousin's WhatsApp forward about floods in a neighbouring state makes you wonder, quietly, if your own house is covered for anything at all. Most Indian homeowners buy a home loan, then completely forget that the asset backing it, their house, sits uninsured for years. Bharat Griha Raksha changed that equation. It is the government-mandated, standardised home insurance policy that every general insurer in India has to sell, built specifically so a homeowner in Coimbatore and one in Guwahati are reading the same policy wording, at broadly comparable prices. This article walks through what it covers, what it leaves out, what it costs, and how to actually buy one without getting confused by insurer jargon.

Table of Contents

- What Is Bharat Griha Raksha Policy?

- Why This Policy Exists in the First Place

- What Does Bharat Griha Raksha Cover?

- What's Not Covered: Exclusions of Bharat Griha Raksha

- Types of Bharat Griha Raksha Cover You Can Choose

- Optional Covers and Add-ons

- How Much Does Bharat Griha Raksha Cost?

- Who Should Buy Bharat Griha Raksha?

- How to Buy a Bharat Griha Raksha Policy

- Bharat Griha Raksha vs Regular Home Insurance Plans

What Is Bharat Griha Raksha Policy?

Bharat Griha Raksha is a standard home insurance product designed by the Insurance Regulatory and Development Authority of India, better known as IRDAI. It was notified on 4th January 2021, and IRDAI made it compulsory for every general insurance company in the country to offer it starting 1st April 2021. Before this, home insurance in India was a mess of differently worded policies from different insurers, each with its own exclusions and fine print, which made comparing plans genuinely difficult.

The idea behind Bharat Griha Raksha was simple. Give every insurer the same base wording, so the product itself cannot be diluted, and let insurers compete on price and service instead of hidden clauses. That is why the coverage terms of Bharat Griha Raksha from HDFC ERGO, Bajaj General Insurance, or SBI General look nearly identical on paper, even though the premiums and add-on options differ.

Why This Policy Exists in the First Place

India experiences recurring losses to residential property due to floods, cyclones, fires and other natural catastrophes, while home insurance penetration remains relatively low. IRDAI's own reasoning for introducing a standard product was to fix two problems at once: confusing policy language that discouraged people from buying cover, and a market where under-insurance was common because homeowners genuinely did not understand what they were paying for.

We have seen this play out with our own customers at SMC. A large number of people who come to us for home insurance are first-time buyers, often triggered by a bank asking for it alongside a home loan, and they rarely know the difference between a structure-only plan and one that also protects their belongings. Bharat Griha Raksha removes a lot of that confusion because the base wording is fixed by regulation, not by the insurer's marketing team.

What Does Bharat Griha Raksha Cover?

The policy is built around two broad components, and you can buy either one alone or both together.

Home Structure Cover

This protects the physical building itself, meaning walls, roof, flooring, and permanent fixtures like wiring and

plumbing, along with any additional structures mentioned in your policy schedule, such as a boundary wall or garage.

If your house suffers a total loss, the insurer pays out based on reconstruction cost, not the market value of

the land. Architect and surveyor fees, debris removal cost, and even rent for alternate accommodation if your

home becomes unliveable are typically built into this cover, subject to the sub-limits in your policy document.

Home Contents Cover

This one protects what is inside the house, your furniture,

appliances, clothes, and everyday belongings, against the same list of insured perils. Tenants find this section particularly

useful since they usually have no stake in the building itself but plenty riding on their possessions. High-value

items like jewellery or art typically need a separate optional cover on an agreed value basis,

since the standard contents cover has its own limits.

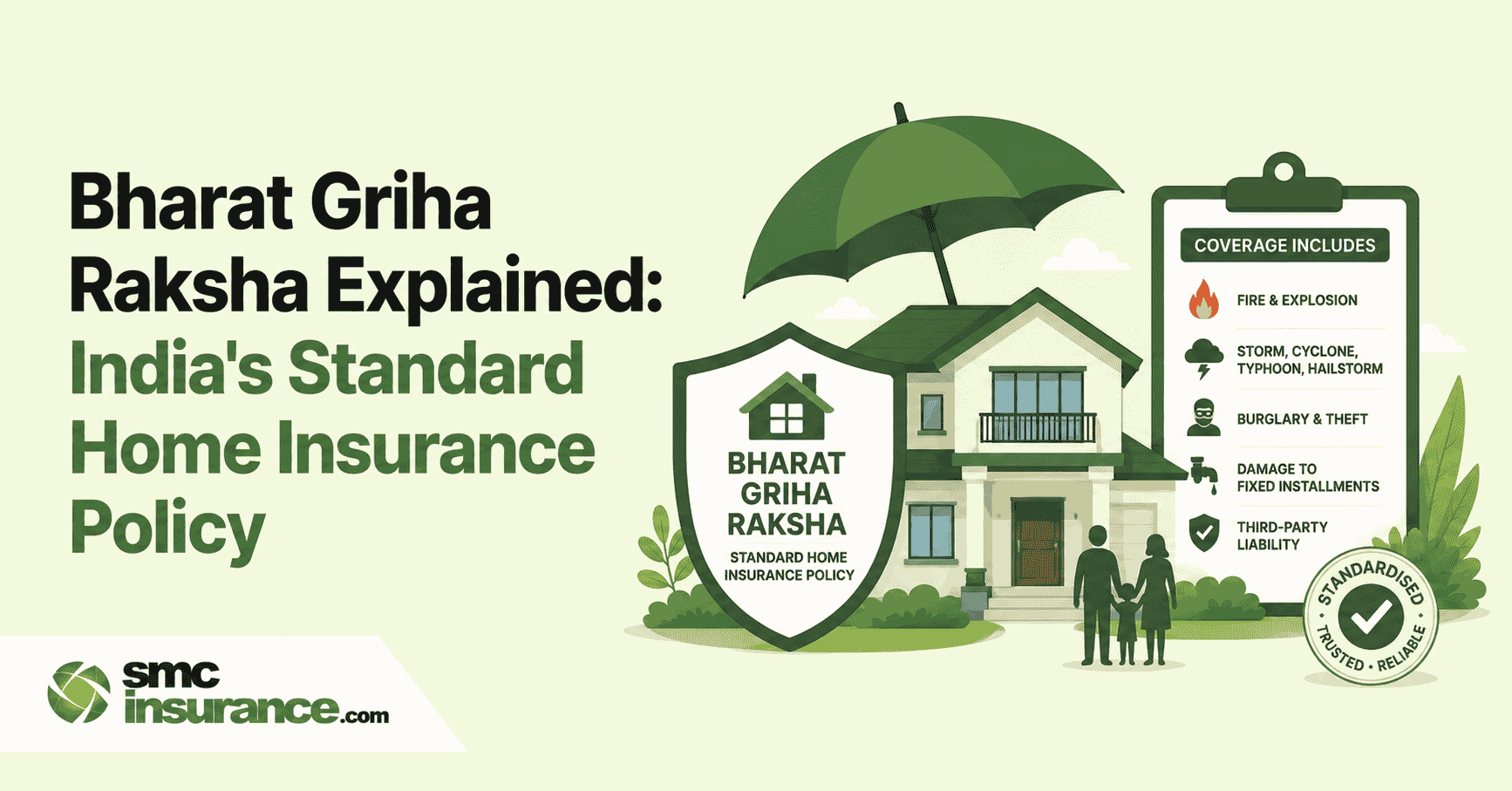

The Perils Covered

Bharat Griha Raksha protects against a long list of events, and this list is what makes it genuinely comprehensive

compared to older fire-only policies. It includes fire, explosion, and implosion; lightning, earthquake,

and volcanic eruption; storms, cyclones, typhoons, tempests, hurricanes, and tornadoes; floods and inundation;

landslides, rockslides, and land subsidence; forest and bush fires; impact damage from a falling tree,

vehicle, or aircraft; missile testing operations; riots, strikes, and acts of terrorism; bursting of

water tanks and pipes; leakage from automatic sprinklers; and theft occurring within seven days of any of the above events actually happening.

That last point trips people up. Bharat Griha Raksha is not a general anti-theft policy on its own.

Theft cover under the base policy is linked to one of the other insured perils occurring first, such as a

fire or storm creating an opportunity for theft. If you want standalone burglary protection, most insurers offer it as an add-on.

What's Not Covered: Exclusions of Bharat Griha Raksha

No policy covers everything, and knowing the gaps upfront saves you from a rejected claim later. The standard exclusions include intentional damage or loss caused by wilful negligence, damage arising from war, invasion, act of foreign enemy, hostilities, civil war and similar war-related events, loss to manuscripts and unlisted precious stones, the cost of pursuing the claim itself, and damage to electronic items caused purely by short circuits or voltage fluctuation rather than an insured peril. Wear and tear, gradual deterioration, and pre-existing structural issues are also outside the scope of this policy, as they would be with any property insurance product.

Types of Bharat Griha Raksha Cover You Can Choose

You are not locked into one shape of policy here. There are three practical combinations available under Bharat Griha Raksha.

- Structure only: Suitable if you own the home but rent it out, since your tenant's belongings are their own responsibility.

- Contents only: Built for tenants, or for owners who already have structure cover through a builder or society policy and just want their belongings protected.

- Structure plus contents: The comprehensive option, and the one most owner-occupied households end up choosing, since it covers both the building and everything inside it under one policy.

If you are still weighing this decision against other home insurance products in the market, it helps to first understand the broader types of home insurance policies in India, since Bharat Griha Raksha is one option among a few standardised and non-standardised covers available to homeowners.

Optional Covers and Add-ons

Beyond the base policy, insurers are allowed to offer optional add-ons that policyholders can choose depending on their risk profile.

- Valuable contents on agreed value basis: For jewellery, art, or antiques where you and the insurer agree on a value upfront using supporting documentation, so a claim does not turn into a valuation dispute later.

- Personal accident cover: If an insured peril also causes the death of the policyholder or their spouse, a lump sum compensation is paid to the nominee, and this benefit typically continues for the surviving spouse until the policy expires.

- Burglary and theft add-on: For standalone protection against theft that is not linked to a preceding insured event.

- Sum insured escalation: Some insurers offer an escalation clause that automatically increases the sum insured, commonly by 10% each year, subject to the product terms.

Add-on availability and pricing differ by insurer, so it is worth asking your advisor exactly which ones are bundled versus charged separately before you sign up.

How Much Does Bharat Griha Raksha Cost?

This is usually the first question people ask, and the honest answer is that it depends heavily on your sum insured, location, and whether you opt for structure only, contents only, or both. That said, here is a broad sense of where premiums typically land, based on publicly disclosed insurer pricing and SMC's own market data.

|

Coverage Type |

Approximate Sum Insured |

Indicative Annual Premium |

|

Basic structure only |

Rs. 11 lakh |

Starting around Rs. 250 with applicable discounts |

|

Structure + contents (mid-range home) |

Rs. 40 lakh structure + Rs. 5 lakh contents |

Roughly Rs. 2,000 to Rs. 4,000 |

|

Comprehensive cover with add-ons |

Higher-value homes |

Roughly Rs. 2,000 to Rs. 10,000, depending on value, location, and add-ons |

Note: These figures are indicative estimates drawn from publicly available insurer pricing and SMC's market access. Actual premiums vary by insurer, property specifics, risk zone, and the add-ons you select, so treat this table as a starting reference rather than a quote.

Premiums also move with your city's risk classification. A home in a flood-prone or seismic zone will naturally cost more to insure than one in a lower-risk area, even at the same sum insured. If you want a fuller breakdown of pricing across property values, our detailed guide on how much home insurance costs covers this in more depth.

Confused about which sum insured actually makes sense for your house? That is exactly the kind of question our advisors at SMC field every day, and comparing quotes from multiple insurers before you buy is the surest way to avoid overpaying. Visit www.smcinsurance.com to compare Bharat Griha Raksha quotes and get a policy that matches your home's actual value.

Who Should Buy Bharat Griha Raksha?

Practically anyone with a financial stake in a residential property. Homeowners obviously top the list, especially those who took a home loan and want their biggest asset protected against the events that could wipe out years of savings in one incident. Tenants are just as eligible, and the contents-only option was designed with exactly this group in mind. Owners who rent out their property should also consider structure cover even though they are not living there, since the building itself remains their liability. Flats, villas, and independent houses are all eligible for coverage, which makes this genuinely one of the more inclusive products in the general insurance space.

How to Buy a Bharat Griha Raksha Policy

The process is fairly quick once you have your property details ready.

Step 1: Decide your cover type: Structure only, contents only, or both, based on whether you own or rent, and whether you already have some cover through a society or builder policy.

Step 2: Estimate your sum insured: For structure, this is usually based on construction cost per square foot, not market value. For contents, list out major belongings and their approximate replacement value.

Step 3: Compare quotes across insurers: Since the base wording is standardised, price, claim settlement track record, and add-on flexibility are what actually differentiate insurers. Comparing a few quotes takes minutes and can meaningfully change what you pay.

Step 4: Share basic documents: Typically identity proof, address proof, and property ownership or rental documents, along with photographs of the property in some cases.

Step 5: Pay premium and receive the policy document: Read through the schedule carefully, particularly the sum insured, sub-limits, and any exclusions specific to your insurer, before the free-look period ends.

Step 6: Renew before expiry: Bharat Griha Raksha does not renew automatically in most cases, so set a reminder well before the policy lapses to avoid a coverage gap.

Bharat Griha Raksha vs Regular Home Insurance Plans

|

Aspect |

Bharat Griha Raksha |

Non-standard/Regular Home Insurance |

|

Policy wording |

Standardised by IRDAI, same across insurers |

Varies by insurer, custom wording |

|

Ease of comparison |

High, since base cover is identical |

Lower, since terms differ significantly |

|

Perils covered |

Wide, fixed list including terrorism |

Depends on insurer and plan chosen |

|

Add-ons |

Available but insurer-specific |

Often more elaborate, insurer-driven |

|

Best suited for |

First-time buyers, tenants, straightforward homes |

High-value homes needing customised, higher-limit cover |

Note: This comparison reflects general market positioning as of 2026. Always check the specific policy wording of any non-standard product before assuming broader coverage, since some regular plans do offer higher sum insured ceilings for premium homes.

If you are comparing insurers rather than just products, our roundup of the best home insurance companies in India breaks down how the major players stack up on claim settlement and pricing.

Summing Up

Bharat Griha Raksha solved a real problem in the Indian home insurance market: confusing, inconsistent policies that discouraged people from buying cover at all. Because the wording is fixed by IRDAI, you know exactly what you are getting regardless of which insurer you pick, and the choice comes down to price, service, and the add-ons that matter to your situation. Whether you own a flat in the city or rent a house with a family, there is a version of this policy built for you, and the entry premiums are low enough that skipping it is rarely a smart financial call. Work out your sum insured honestly, compare a few quotes, and get your home covered before the next monsoon or the next unexpected short circuit makes the decision for you.

Disclaimer: The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or government-specific modifications. Readers should verify current terms and conditions directly with relevant government departments or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product's suitability. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Applicants are advised to review official policy documents and insurer disclosures before proceeding with any purchase.

FAQs

It is a standard home insurance policy introduced by IRDAI in January 2021 and made mandatory for all general insurers to offer from April 2021. It covers your home structure, contents, or both against fire, natural disasters, theft linked to insured perils, and terrorism, using the same base wording across every insurer in India.

No, buying it is not compulsory for homeowners. What is mandatory is that every general insurance company must offer this product. Some banks may ask for basic structure cover when you take a home loan, but that requirement comes from the lender, not from IRDAI.

Coverage tenure is flexible and can go up to 10 years in a single policy, depending on what the insurer offers and what you choose at the time of purchase.

Yes, but only theft that occurs within seven days of another insured peril, like a fire or storm. Standalone burglary protection, unconnected to any other event, usually needs to be added as a separate optional cover.

Yes, tenants can buy the contents-only version of the policy to protect their belongings, since they typically have no insurable interest in the building structure itself.

Intentional damage, war-related losses, damage to manuscripts and unlisted precious stones, claim-processing costs, and short-circuit damage to electronics are among the standard exclusions. Always check your specific policy schedule for insurer-added exclusions.

Generally no. Most insurers require manual renewal before the policy expires, so it is worth setting a calendar reminder to avoid a lapse in coverage.

For the structure, sum insured is typically based on construction cost per square foot rather than market value or land price. For contents, it is based on the estimated replacement value of your belongings.