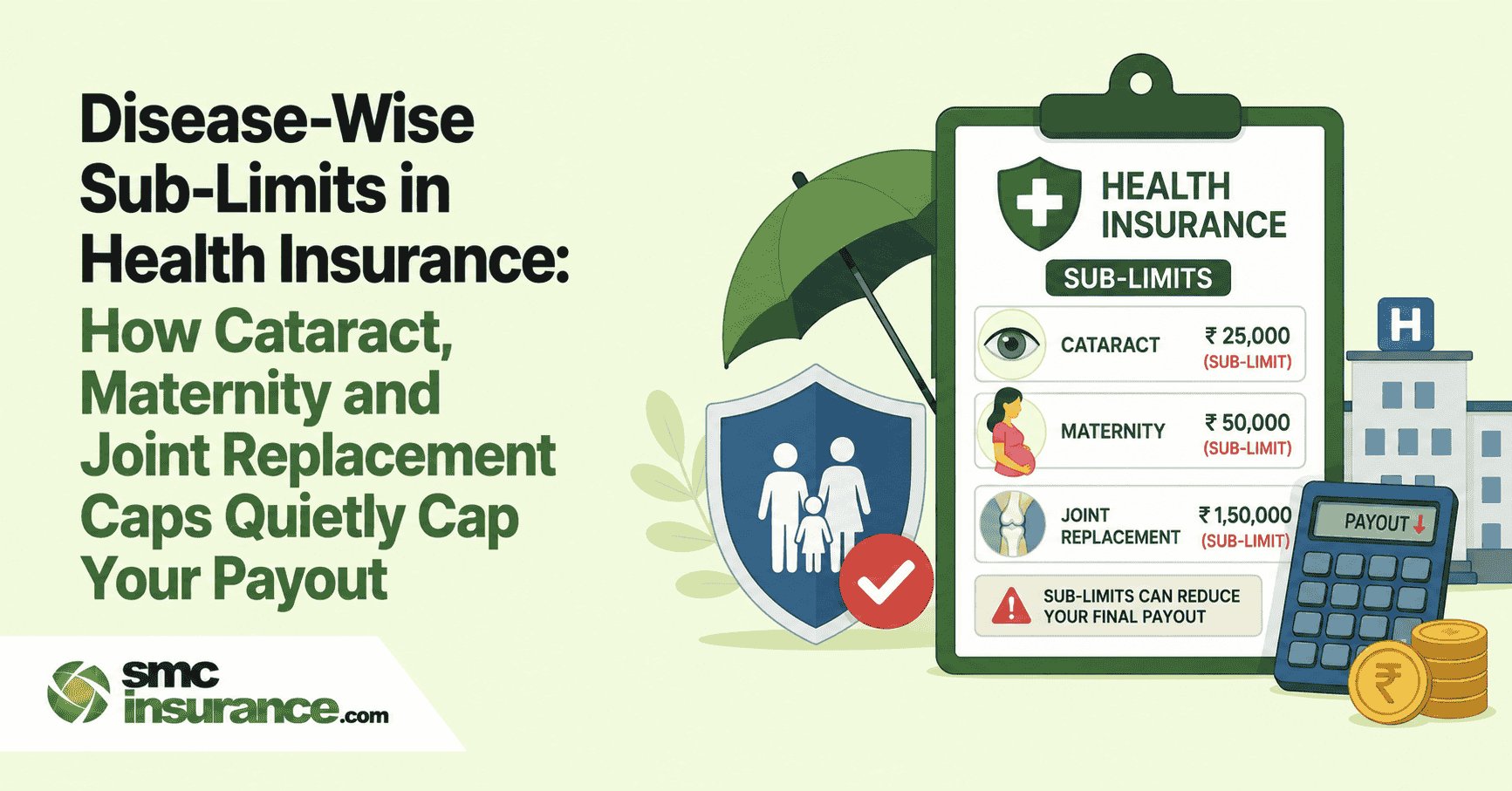

A disease-wise sub-limit caps what your insurer pays for a specific treatment, regardless of your total sum insured. Cataract is commonly capped at Rs. 20,000 to Rs. 50,000 per eye in many health insurance plans, while maternity benefits are often subject to policy-specific limits ranging from around Rs. 15,000 for normal delivery in basic plans to Rs. 1,50,000 for caesarean delivery in some premium plans. Some insurers also impose fixed limits on joint replacement procedures, even though actual surgery costs may range from around Rs. 1.5 lakh to Rs. 6 lakh depending on the hospital, implant and city. Check your Customer Information Sheet for the exact figures and consider a no-sub-limit plan if these procedures are likely in your family's future.

Rajesh bought a Rs. 10 lakh health policy three years ago and felt fully covered. Then his cataract surgery bill came in at Rs. 55,000 per eye and the insurer settled only Rs. 30,000. The rest came out of his own pocket, even though his sum insured had barely been touched. This is what a disease-wise sub-limit does. It sits quietly inside the policy wording, capping specific treatments like cataract, maternity and joint replacement, regardless of how large your overall cover looks on paper. By the end of this article, you will know exactly where these caps show up, what amounts insurers typically apply and how to check your own policy before you are the one standing at the billing counter with an unexpected shortfall.

Table of Contents

- What Is a Disease-Wise Sub-Limit and Why It Differs From Room Rent Caps

- The Cataract Sub-Limit: India's Most Common Surgery, Its Most Common Cap

- Maternity Sub-Limits: Why a Rs. 10 Lakh Policy Can Still Pay Only Rs. 50,000 for Delivery

- Joint Replacement and Knee Surgery: The Cap That Surprises Older Policyholders Most

- Typical Disease-Wise Sub-Limits by Plan Tier

- How the 2024 IRDAI Master Circular Changed What Insurers Must Disclose

- How to Check Your Policy for Disease-Wise Sub-Limits

- Protecting Yourself Before the Claim, Not After

What Is a Disease-Wise Sub-Limit and Why It Differs From Room Rent Caps

A sub-limit is a predefined ceiling on what an insurer will pay for a specific treatment and it applies even when the total sum insured is far from exhausted. Under the IRDAI Master Circular on Health Insurance Business, a sub-limit is defined as a cost-sharing arrangement under which the insurer is not liable to pay any amount beyond a pre-set figure, whether that figure is a fixed rupee amount or a percentage of the sum insured.

Room rent limits get most of the attention because a single upgraded hospital room can trigger a proportionate deduction across the entire bill. Disease-wise sub-limits work differently. They target a named procedure, such as cataract surgery, delivery expenses or joint replacement and cap that specific claim on its own, independent of how the rest of the hospitalisation is billed. A policyholder can have zero room rent issues and still walk away with a five-figure shortfall purely because the procedure itself was capped. We have seen this catch out even careful buyers who read the room rent clause closely but skipped the disease-wise annexure entirely.

The Cataract Sub-Limit: India's Most Common Surgery, Its Most Common Cap

Cataract is the single most frequently claimed procedure in Indian health insurance and it is also the one insurers are most inclined to cap. Many traditional retail and group health insurance policies impose cataract sub-limits, commonly ranging between Rs. 20,000 and Rs. 50,000 per eye, although several newer comprehensive plans have removed these limits altogether. Group health policies commonly restrict this to Rs. 20,000 to Rs. 40,000 per eye.

The gap between this cap and actual treatment cost is where the trouble starts. Standard phacoemulsification surgery at a private hospital typically costs Rs. 40,000 to Rs. 60,000 per eye and bladeless laser-assisted procedures can run from Rs. 85,000 up to Rs. 1,20,000 per eye. A policyholder choosing a metro hospital and a slightly advanced technique can end up paying the difference entirely from their own pocket, even while their overall sum insured remains almost untouched. Two other details compound this:

- First, premium intraocular lenses such as multifocal or toric lenses are generally reimbursed only up to the cost of a standard monofocal lens, so upgrading the lens adds another layer of out-of-pocket cost.

- Second, cataract usually carries a specific-illness waiting period of 12 to 24 months and a longer pre-existing disease waiting period applies if the condition was diagnosed before the policy was bought. Basic micro and rural plans push the cap even lower, sometimes to around Rs. 10,000 to Rs. 15,000 per eye.

Several comprehensive health insurance products available in the market now offer cataract coverage up to the full sum insured without a disease-specific sub-limit. Since this varies by insurer and product variant, always verify the Customer Information Sheet and policy wording before purchase. That single feature is worth checking before you assume every plan behaves the same way. We generally tell clients shopping for senior citizen cover to treat the cataract clause as a decisive factor, since it is almost always the first claim a policy over the age of 55 will see.

Maternity Sub-Limits: Why a Rs. 10 Lakh Policy Can Still Pay Only Rs. 50,000 for Delivery

Maternity works as a built-in benefit or a paid rider on most family floater and group policies and it almost always carries its own separate cap that has nothing to do with the base sum insured. Basic plans typically cover normal delivery in the range of Rs. 15,000 to Rs. 50,000, while caesarean delivery is capped somewhere between Rs. 25,000 and Rs. 1,00,000. Mid-range and premium plans push these figures higher, with some premium products offering caesarean cover up to Rs. 1,50,000, but the cap remains a cap regardless of tier.

A normal delivery at a private hospital in a metro city can cost anywhere from Rs. 60,000 to Rs. 1.5 lakh and a caesarean section can climb to Rs. 2 lakh to Rs. 5 lakh depending on complications and the hospital chosen. Against those figures, a Rs. 50,000 maternity sub-limit covers only a fraction of the real bill in a tier-1 city, even though it might comfortably handle a straightforward delivery in a smaller town.

Corporate group policies add another wrinkle. Many employer-provided plans cap the maternity rider at Rs. 50,000 regardless of the base sum insured offered to employees, since this is a common ceiling written into group underwriting terms. Newborn cover is generally linked to the mother's approved maternity claim, but the duration of automatic coverage varies by insurer. Most policies require the newborn to be formally added to the policy within the timeline specified in the policy wording. Waiting periods for maternity are also unusually long, ranging from 9 months to 4 years depending on the insurer, so this is not a benefit you can add once pregnancy is already confirmed.

Joint Replacement and Knee Surgery: The Cap That Surprises Older Policyholders Most

Knee and hip replacement surgeries sit in a category where the treatment cost itself varies enormously, anywhere from around Rs. 1.5 lakh to Rs. 6 lakh depending on the implant, the hospital and whether robotic assistance is used. Insurers that impose disease-wise sub-limits on orthopaedic procedures typically fix a rupee ceiling for the surgery that does not move with the rest of your sum insured, which becomes a serious gap given how wide the actual cost range is.

Implants are frequently the hidden trigger here. Even where the surgery itself is covered generously, many policies pay only for a standard implant and the difference for an imported or premium implant has to be paid by the patient. This is separate from and in addition to, any procedure-level sub-limit that might already apply. Joint replacement also carries a specified-illness waiting period of 24 months in most policies, extending to 36 months if arthritis or joint degeneration was diagnosed before the policy was purchased.

As with cataract, several higher-tier comprehensive plans now explicitly remove sub-limits on joint replacement and pay up to the full sum insured. This is one of the clearest tests for whether a policy is genuinely comprehensive or only comprehensive on the surface, since orthopaedic claims are among the largest single-procedure bills a senior citizen policy is likely to face.

Typical Disease-Wise Sub-Limits by Plan Tier

|

Procedure |

Basic Plans |

Mid-Range Plans |

Premium / No-Sub-Limit Plans |

Cataract (per eye) |

Rs. 10,000 – Rs. 30,000 |

Rs. 30,000 – Rs. 50,000 |

Full sum insured |

Normal Delivery |

Rs. 15,000 – Rs. 25,000 |

Rs. 25,000 – Rs. 50,000 |

Rs. 50,000 – Rs. 1,00,000 or full SI |

Caesarean Delivery |

Rs. 25,000 – Rs. 40,000 |

Rs. 50,000 – Rs. 75,000 |

Rs. 75,000 – Rs. 1,50,000 or full SI |

Joint Replacement |

Fixed rupee cap, often below actual cost |

Higher fixed cap, implant limits apply |

Full sum insured |

Note: These are indicative ranges compiled from publicly available insurer disclosures and industry reporting. Exact figures vary by insurer, product variant and city and depend on the sum insured you select. Always confirm the applicable sub-limits in your policy's Customer Information Sheet and policy schedule before relying on these figures.

Planning a pregnancy, an aging parent's cataract surgery, or already anticipating a knee replacement in the family? These are exactly the moments where a sub-limit clause decides how much you actually pay. Talk to an advisor at SMC Insurance to compare policies that either raise these caps significantly or remove them altogether.

How the 2024 IRDAI Master Circular Changed What Insurers Must Disclose

The Master Circular on IRDAI (Insurance Products) Regulations 2024 for Health Insurance, dated 29 May 2024, tightened how insurers define and disclose sub-limits. Every policyholder is now entitled to a standardised Customer Information Sheet under Regulation 26 of the IRDAI (Health Insurance) Regulations, 2016 and the revised CIS format has applied since 1 January 2024. The sheet must state financial limits of coverage, including sub-limits, co-payments and deductibles, in plain language with a minimum font size and insurers must obtain the policyholder's acknowledgement of having received it.

The 2024 regulatory framework strengthened the standardisation and disclosure of health insurance benefits, including the presentation of financial limits through the Customer Information Sheet. It also requires insurers to make health insurance products available for AYUSH treatments in accordance with applicable regulations, although coverage continues to depend on the policy terms. The moratorium period, after which insurers cannot contest a claim on grounds of non-disclosure except proven fraud, has been reduced to 60 continuous months and the maximum pre-existing disease waiting period has been brought down as part of the same standardisation exercise. None of this removes disease-wise sub-limits on cataract, maternity or joint replacement by default. It simply forces insurers to state those caps clearly instead of burying them in dense policy wording, which makes the CIS the fastest place to check before you buy.

How to Check Your Policy for Disease-Wise Sub-Limits

1: Pull out your Customer Information Sheet

It is a one to two page document every insurer must issue and it lists financial limits of coverage in a standard format.

2: Look specifically for a "sub-limits" or "disease-wise limits" table

It will separately list room rent, cataract, maternity and any other capped procedures rather than bundling them together.

3: Compare the rupee figure against real treatment costs in your city

A Rs. 30,000 cataract cap means very little without knowing that private hospitals in your city charge Rs. 45,000 or more for the

same surgery.

4: Check whether the cap is a fixed amount or a percentage of sum insured

A percentage-based cap on a low sum insured policy can be lower than a flat cap on a basic plan, so read the fine print rather than

assuming a bigger sum insured always means a bigger disease payout.

5: Ask directly whether the plan offers a no-sub-limit variant

Several insurers sell a base product with caps and a higher-premium variant without them and the difference is not always obvious

from the brochure alone.

Protecting Yourself Before the Claim, Not After

The most reliable fix is buying a plan that removes disease-wise sub-limits altogether, especially if your family history points toward cataract, planned maternity, or joint issues later in life. Where that pushes the premium beyond budget, at minimum compare the specific rupee caps across two or three insurers rather than comparing sum insured alone, since two Rs. 10 lakh policies can behave very differently at the claim stage. Reading the disease-wise annexure before buying takes a few extra minutes. Discovering the cap at the hospital billing counter costs a great deal more.

Summing Up

Sub-limits on cataract, maternity and joint replacement do not show up in the headline sum insured figure, yet they decide how much of a real hospital bill your insurer actually pays. Cataract caps commonly fall between Rs. 20,000 and Rs. 50,000 per eye against real costs that often exceed that range. Maternity caps can leave a metro delivery bill only partially covered. Joint replacement caps struggle to keep pace with a cost range that stretches into lakhs. The IRDAI-mandated Customer Information Sheet now makes these figures easier to find than ever, so the responsibility shifts to actually reading it before you sign. Compare the disease-wise annexure, not just the sum insured and where possible, choose a policy that removes these caps for the treatments your family is most likely to need.

Disclaimer: The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product's performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents and disclosures before proceeding with any purchase or commitment.

FAQs

A disease-wise sub-limit is a cap an insurer places on how much it will pay for a specific treatment, such as cataract surgery, delivery expenses or joint replacement. It applies regardless of your total sum insured, so a large policy can still pay only a fixed amount for that particular procedure.

Most policies cap cataract surgery between Rs. 20,000 and Rs. 50,000 per eye, while group health policies often restrict it further to Rs. 20,000 to Rs. 40,000 per eye. Actual surgery costs at private hospitals commonly range from Rs. 40,000 to Rs. 60,000 per eye, so the gap can be significant.

Yes, basic plans typically cap normal delivery between Rs. 15,000 and Rs. 25,000 and caesarean delivery between Rs. 25,000 and Rs. 40,000. Premium plans offer higher caps, sometimes up to Rs. 1,50,000 for caesarean delivery, but a cap almost always exists unless the plan is specifically marketed as having no maternity sub-limit.

Many policies apply a fixed rupee cap on joint replacement that does not scale with your sum insured, even though actual surgery costs can range from Rs. 1.5 lakh to Rs. 6 lakh. Implant costs beyond a standard implant are usually an additional exclusion on top of any procedure sub-limit.

Several insurers offer higher-tier plans or add-ons that remove sub-limits on cataract, maternity and joint replacement entirely, paying up to the full sum insured instead. This typically comes at a higher premium, so it is worth comparing the cost difference against your likely claim exposure.

Yes, under the IRDAI Master Circular on Health Insurance Business, 2024, every insurer must provide a standardised Customer Information Sheet that clearly states sub-limits, co-payments and deductibles in plain language and obtain the policyholder's acknowledgement of receiving it.

Check your Customer Information Sheet or policy schedule for a section listing financial limits of coverage. It should separately state caps for room rent, cataract, maternity and other named procedures rather than bundling them under one figure.

No, room rent limits cap your daily hospital room charge and can trigger a proportionate deduction across your entire bill if exceeded. Disease-wise sub-limits cap a specific procedure's claim amount on its own, independent of the room you choose.