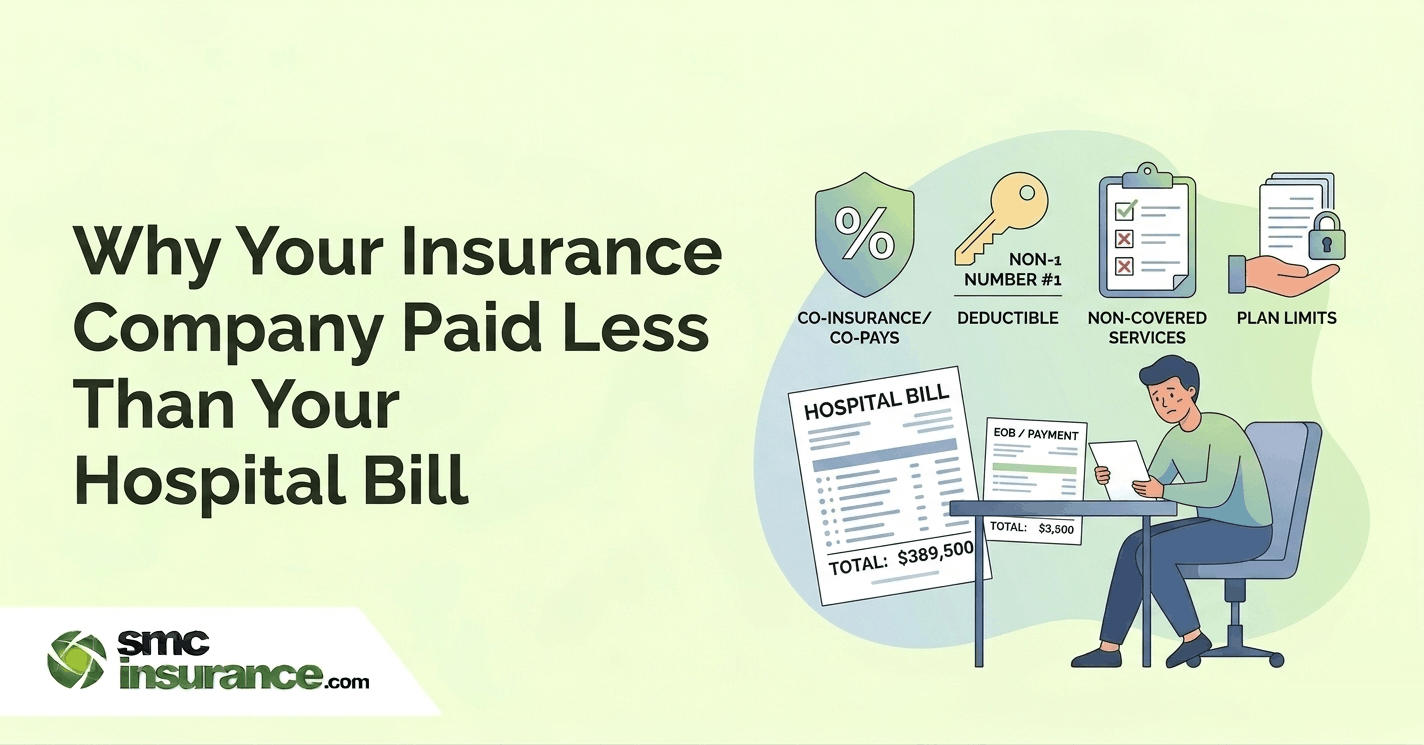

Why did the insurance company pay less than my hospital bill?

Health insurers pay less than the total hospital bill because of specific policy conditions: room rent caps (which trigger proportionate deductions on other charges), sub-limits on treatments like cataract or knee replacement, co-pay clauses, exclusions for non-payable consumables like gloves and syringes and the Reasonable and Customary clause at non-network hospitals. As per IRDAI's own findings in 2025, settled claim amounts are frequently lower than what policyholders expect, even when the claim is technically approved. To receive a higher payout, choose policies with no room rent cap, no sub-limits, zero co-pay and a consumables rider. If you believe your insurer under-settled your claim, escalate via IRDAI's Bima Bharosa portal or the Bima Lokpal.

You come home from the hospital, relieved the treatment went well. Then the settlement summary arrives. Your bill was Rs. 3.5 lakh. Your insurer settled Rs. 2.1 lakh. The remaining Rs. 1.4 lakh is yours to arrange, right now, from savings you weren't planning to touch. No one warned you. No one explained what would be deducted or why.

This is not an isolated case. The IRDAI chairman, Ajay Seth, flagged this exact problem publicly in 2025: high claim settlement ratios look good on paper, but they hide the fact that the actual amount paid out is far lower than what policyholders expected. A claim being "approved" and a claim being "fully paid" are two very different things, and most people only learn this difference at the worst possible time.

This article breaks down every reason your insurer may have paid less than your hospital bill, what you can do about it right now and how to stop it from happening in your next policy.

7 Reasons Your Insurance Company Paid Less Than Your Hospital Bill

The gap between what the hospital charges and what the insurer settles is almost never random. Each deduction traces back to a specific clause in your policy. Here are the most common ones.

1. Room Rent Capping: The Hidden Multiplier

Room rent capping is the single biggest reason policyholders get blindsided. Most policies cover room rent only up to a fixed limit, say 1% of the sum insured per day. If your sum insured is Rs. 5 lakh, your room rent cap is Rs. 5,000 per day.

The real damage happens when you upgrade to a room that costs Rs. 8,000 per day. Your insurer doesn't just reduce the extra Rs. 3,000. It proportionately reduces a range of other charges tied to the room, including surgeon fees, nursing charges and consultation costs. This is called proportionate deduction. A Rs. 3,000 room upgrade can cost you Rs. 40,000 more across the final bill.

The fix is straightforward. Look for policies that say "no room rent capping," "any room," or "single private AC room" with no sub-limit.

2. Sub-limits on Specific Treatments

Many plans impose a fixed cap on certain procedures, regardless of what the hospital actually charges. Cataract surgery is commonly capped at Rs. 40,000 per eye. Knee replacement may have a cap of Rs. 1.5 lakh per knee. Maternity coverage often has its own sub-limit, separate from the overall sum insured.

If your actual cost exceeds these caps, you pay the difference. The insurer does not care what the hospital charged. It pays up to the ceiling it agreed to, no more.

Before buying or renewing a policy, check for sub-limits on treatments you are likely to need. If a sub-limit exists, check whether the cap is realistic based on current hospital costs in your city.

3. Co-payment Clause

A co-pay means you share a fixed percentage of every claim with the insurer. A 10% co-pay on a Rs. 3 lakh bill means you are personally responsible for Rs. 30,000. This applies to every single claim, every single time.

Senior citizen policies frequently carry co-pay clauses, sometimes as high as 20–30%. Policies sold to younger buyers may include co-pay clauses voluntarily to reduce premium costs. Either way, the deduction is non-negotiable once the clause is in the policy.

If affordability is not a concern, always prefer a zero co-pay policy.

4. Non-payable Items and Consumables

This is the most commonly misunderstood deduction. IRDAI has a standard list of items that no health insurer is required to cover. These include gloves, syringes, PPE kits, cotton, hospital gowns, tissues, laundry charges, visitor meals, mineral water, telephone charges and similar items billed by the hospital.

Individually, each item costs Rs. 50 to Rs. 500. Across a five-day hospitalisation with procedures, these add up to Rs. 10,000 to Rs. 30,000 or more. You pay this from your own pocket unless your policy has a consumables cover or non-payables add-on rider.

|

Category of Non-Payable Items |

Common Examples |

|

Room-related incidentals |

Tissues, mineral water, visitor meals, laundry |

|

Consumables used in treatment |

Gloves, syringes, cotton, PPE kits, surgical blades |

|

Optional items (situation-specific) |

Diapers, baby food, sanitary pads, belts/braces |

|

Procedure-related extras |

Surgical blades, sterilisation charges, specimen bags |

|

Hospital charges |

Email/internet charges, telephone charges, guest services |

Note: The IRDAI non-payables list is standard across all insurers. Adding a consumables rider at the time of policy purchase is the only way to cover these costs.

5. Reasonable and Customary Charges Clause

You went to a non-network hospital. You submitted the bills for reimbursement. The insurer approved the claim, but settled only a part of it because the hospital's charges were "above prevailing rates" in your city.

This is the Reasonable and Customary (R&C) clause in action. Insurers maintain internal benchmarks for what a procedure should cost in a given city or region. If your hospital charged more than that benchmark, the excess becomes your liability. The insurer does not disclose these benchmarks in advance, which makes this one of the more frustrating deductions to deal with.

Sticking to network hospitals for cashless treatment is the most reliable way to avoid this. Cashless claims at network hospitals bypass the R&C clause because the insurer and hospital have a pre-agreed rate.

6. Waiting Period Exclusions for Pre-existing Conditions

Health insurance in India typically has a waiting period of two to four years for pre-existing diseases. If you are hospitalized for a condition related to a pre-existing disease and your waiting period has not elapsed, the claim will be partially or fully rejected.

IRDAI's 2024 regulations reduced the maximum waiting period for pre-existing diseases to three years, down from four. Some insurers offer policies with shorter waiting periods, though these typically carry higher premiums.

7. Deductibles

A deductible is a fixed amount you must bear before your insurance kicks in. If your deductible is Rs. 25,000 and your bill is Rs. 80,000, the insurer settles Rs. 55,000. The first Rs. 25,000 is yours.

Deductibles are sometimes bundled into plans with lower premiums as a trade-off. They make sense for people who rarely hospitalise but want protection against large, catastrophic bills. For frequent hospitalisation, a deductible can be expensive.

What the Claim Settlement Ratio Does Not Tell You

The Claim Settlement Ratio (CSR) is the percentage of claims that get approved. A CSR of 98% sounds excellent. Most policyholders read this as reassurance that their claim will be paid.

What CSR does not tell you is how much was paid versus how much was claimed. An insurer can approve 98% of all claims and still settle each one at 60–70% of the actual bill. The metric counts approvals, not amounts.

The IRDAI has acknowledged this gap and is working on frameworks to make insurers more transparent about settlement amounts. Until then, do not use CSR alone as a measure of insurer quality. Ask about claim rejection rates and average settlement ratios when comparing policies.

When Your Insurer Has Deducted More Than They Should

Not every deduction is legitimate. If you believe the insurer has over-deducted or applied a clause incorrectly, you have a clear escalation path.

Step 1: Request a detailed deduction note from your insurer

Every deduction must be explained clause by clause. A vague reply citing "policy conditions" is not acceptable.

Step 2: Raise a formal written grievance with your insurer's Grievance Redressal Officer (GRO)

The insurer must respond within 15 days.

Step 3: If unresolved, escalate to IRDAI's Bima Bharosa portal

This can be done at bimabharosa.irdai.gov.in. Launched by IRDAI in 2022, Bima Bharosa is the official grievance redressal platform. Your complaint gets a unique token number and is visible to IRDAI for monitoring. As per IRDAI's Master Circular on Policyholder Protection 2024, all non-cashless claims must be settled within 15 days of receipt.

Step 4: If still unresolved, approach the Bima Lokpal (Insurance Ombudsman)

The Ombudsman provides free, impartial resolution of disputes between policyholders and insurers. This service is free of charge. In FY 2024-25, 69% of insurance sector grievances registered on Bima Bharosa were claim-related, which shows how common this problem is.

|

Escalation Level |

Body |

Timeframe |

|

Level 1 |

Insurer's Grievance Redressal Officer (GRO) |

15 days |

|

Level 2 |

IRDAI Bima Bharosa Portal |

15 days after insurer non-response |

|

Level 3 |

Bima Lokpal / Insurance Ombudsman |

Free, independent resolution |

|

Level 4 |

Consumer Forum / Civil Court |

Legal recourse as last resort |

Note: You can contact the IRDAI Grievance Call Centre toll-free, or write to complaints@irdai.gov.in. Always keep all communication and documents in writing.

Struggling with a partial claim settlement you cannot explain? The right broker can help you read your deduction note, identify what was wrongly withheld and escalate effectively. Visit SMC Insurance to connect with an advisor who can walk you through your claim, clause by clause.

How to Choose a Policy That Pays More of Your Bill

Fixing a bad policy at the time of claim is hard. Choosing a better one upfront is far easier.

|

Feature to Check |

What to Look For |

What to Avoid |

|

Room rent |

No cap / Any room / Single private AC |

Percentage-based or fixed daily limit |

|

Sub-limits |

None on specific treatments |

Per-event caps on procedures |

|

Co-payment |

Zero co-pay |

Any co-pay above 10% |

|

Consumables |

Inbuilt cover or add-on available |

No consumables rider option |

|

Network hospitals |

Wide network in your city |

Narrow network limited to select hospitals |

|

Pre-existing waiting period |

1 to 2 years |

3 to 4 years |

Note: Policies with no room rent cap, no sub-limits and zero co-pay typically carry higher premiums. Compare these against the likely out-of-pocket cost in a partial settlement before deciding.

When comparing policies, look beyond the premium. A plan that costs Rs. 3,000 more per year but covers consumables and removes room rent caps can save you Rs. 50,000 or more in a single hospitalisation.

For those with an existing health policy, consider top-up or super top-up plans to increase coverage without replacing the base policy. These add a deductible-style layer of protection at a lower cost than buying a fresh high-sum-insured policy.

You can read more about health insurance claim types and how to use them to decide whether cashless or reimbursement suits your situation better.

If you are unsure which plan covers what your family actually needs, exploring the best health insurance plans in India with us to compare multiple insurers side by side is the most practical first step.

Wrapping Up,

Insurance approval delays happen for specific, traceable reasons. They are almost never just "the system taking time." Documents are missing, a TPA has not relayed information, a waiting period is being applied, or the claim has triggered an investigation. Knowing which of these applies to your situation puts you back in control.

Keep your documents organised, follow up in writing and do not let phone conversations be your only record. If the claim is genuinely stuck beyond the regulatory timeline, Bima Bharosa and the Insurance Ombudsman exist precisely for this. In FY 2024-25, 7 in 10 ombudsman cases ended in the policyholder's favour. You have more leverage than the waiting room suggests. The key is knowing when to wait, when to ask and when to escalate.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

FAQs

Health insurance rarely covers 100% of every hospital bill. Policies typically exclude certain items as non-payable, apply room rent caps that trigger proportionate deductions, impose sub-limits on specific treatments and include co-pay clauses. The IRDAI chairman flagged in 2025 that high claim settlement ratios often mask the fact that the actual amounts settled are significantly lower than what policyholders claimed. Reading your policy document in advance, particularly the exclusions and limitations sections, is the only reliable way to understand what you will and will not receive.

Non-payable items are a standard list of consumables and incidental expenses that IRDAI has classified as ineligible for coverage under regular indemnity health insurance. These include gloves, syringes, PPE kits, surgical blades, cotton, tissues, mineral water, laundry charges and telephone charges, among others. The list is uniform across all insurers. Policyholders must pay these costs themselves unless they have purchased a consumables cover or non-payables rider as an add-on to their base policy.

Proportionate deduction happens when you occupy a hospital room with a higher rent than your policy allows. The insurer reduces not just the excess room rent but also proportionately scales down other charges linked to the room, including surgeon fees, nursing charges and consultation costs. For example, if your policy covers a Rs. 5,000-per-day room but you chose an Rs. 8,000-per-day room, the insurer applies a 5/8 ratio to several associated charges. This multiplier effect is why room rent capping causes far larger deductions than most policyholders anticipate.

Yes, you can. First, request a clause-by-clause deduction note from your insurer. If you believe any deduction is incorrect or unjustified, raise a formal written grievance with the insurer's Grievance Redressal Officer. They must respond within 15 days. If unresolved, escalate to IRDAI's Bima Bharosa portal. If that also fails, approach the Bima Lokpal (Insurance Ombudsman), which provides free and independent resolution of disputes. Keep all communication in writing, including your original claim documents and the insurer's deduction note.

CSR measures the percentage of claims approved, not the percentage of the billed amount paid. An insurer with a 98% CSR may still routinely settle claims at 65–70% of the actual bill due to policy conditions. The IRDAI has acknowledged that CSR alone does not reflect whether policyholders receive fair value. When evaluating an insurer, also consider average settlement amounts, customer reviews specifically about claim experiences and grievance data available on IRDAI's public reports.

A co-payment means you pay a fixed percentage of every claim. A 10% co-pay on a Rs. 2 lakh bill means you pay Rs. 20,000 and the insurer pays Rs. 1.8 lakh. A deductible is a fixed rupee amount you must bear before the insurer contributes anything. If your deductible is Rs. 50,000 and your bill is Rs. 1.5 lakh, the insurer pays Rs. 1 lakh. Deductibles are common in top-up plans and keep base premiums lower. Co-pays are more common in senior citizen policies or voluntary selections to reduce annual premium costs.

Choose a policy with no room rent capping, no sub-limits on common treatments, zero co-pay and either in-built consumables cover or an available add-on rider. Prefer network hospitals for cashless treatment to avoid the Reasonable and Customary clause. Before admission, verify your room eligibility with the insurer and initiate pre-authorisation. If your current sum insured feels insufficient, a super top-up plan is a cost-effective way to extend coverage without replacing your existing policy.