Your employer's group health insurance ends on your last working day, or whenever your employer's policy states, with no legal obligation to extend it. Your protection is the right to migrate that cover to an individual or family floater policy with the same insurer, keeping your sum insured, bonus and unexpired waiting periods intact, though the new policy is subject to underwriting and usually costs more than your corporate rate. Confirm your exact cover-end date with HR and start the migration or a fresh policy purchase the same week you resign to avoid any gap in coverage.

You get the call on a Tuesday afternoon, or maybe you hand in your resignation letter yourself. Either way, your last working day is fixed and somewhere between clearing your desk and returning your laptop, a question quietly surfaces: what happens to the health insurance your company gave you? For most salaried employees in India, the group health policy that covered hospital bills, ambulance charges and sometimes even a parent's treatment stops the same day the employment does. There is no automatic cushion, no thirty-day countdown that applies to everyone. What you do in the days right after matters more than most people realise and this article walks you through exactly what ends, what you can carry forward and how to make sure a medical emergency during a job transition does not turn into a financial one.

Table of Contents

- Your Group Health Cover Ends the Day Your Employment Does

- Migration, Not Portability, Is Your Real Right Here

- How the Numbers Actually Work Once You Migrate

- Applying for Migration Without Losing Time

- What If Buying a Fresh Policy Makes More Sense

- If Your Cover Came Through ESIC Instead of a Corporate Policy

- Practical Steps to Avoid a Coverage Gap

- Summing Up

Your Group Health Cover Ends the Day Your Employment Does

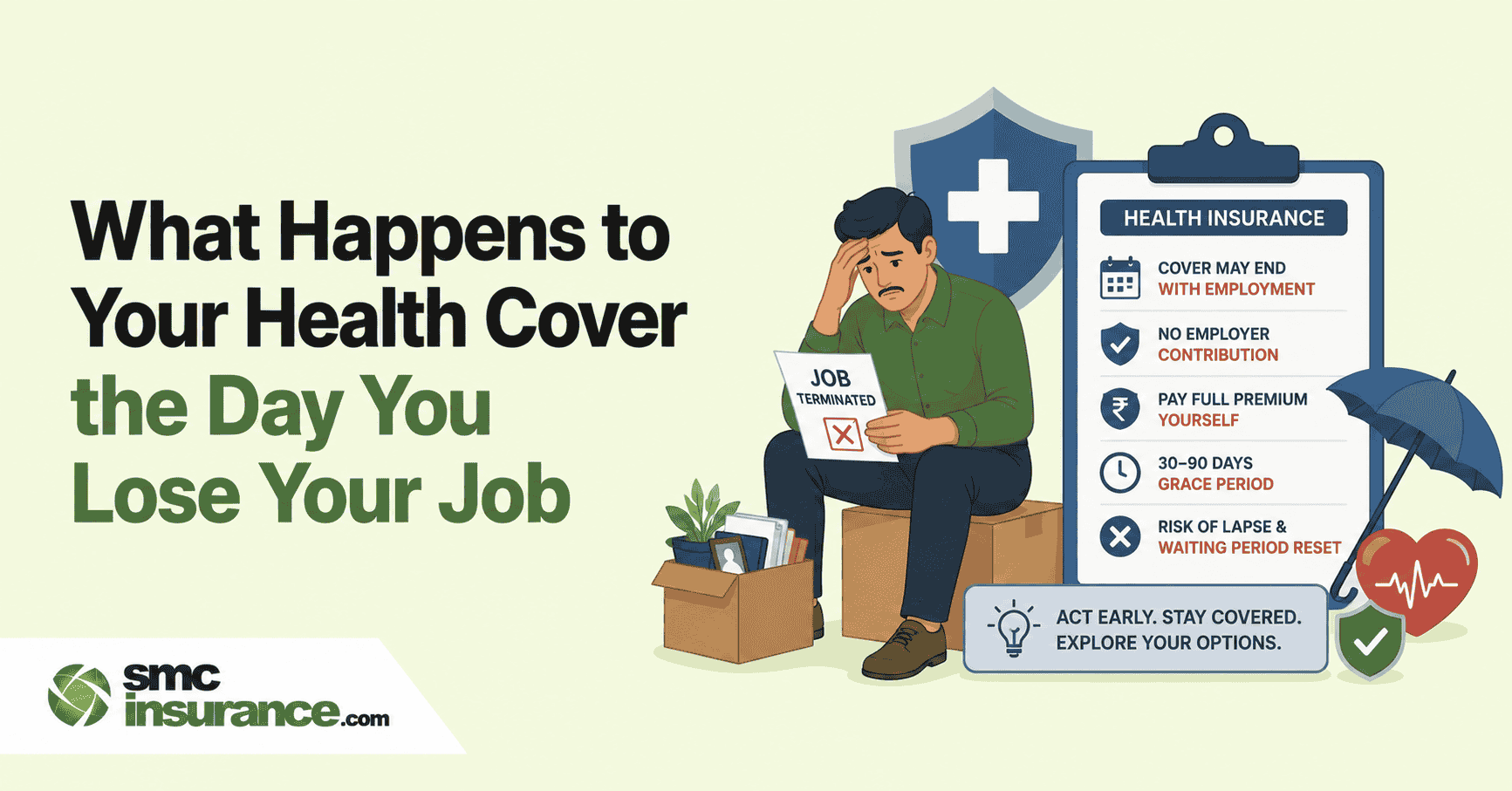

Group health insurance is issued to your employer, not to you. You are added as a member because you work there and the moment that relationship ends, so does your place on the policy. Most insurers write this into the group policy wording itself: cover for an exiting employee stops from the date of resignation, retirement, or termination, or at most till the end of that month, depending on what the employer has negotiated with the insurer.

There is no law in India that forces an employer to extend your health cover after you leave. Some companies build in a short grace period as a goodwill gesture, occasionally stretching to fifteen or thirty days, but this is entirely at the employer's discretion and varies from one HR policy to another. If you are serving a notice period, your cover typically continues until your last working day, not your date of resignation. It is worth asking HR for this in writing rather than assuming, because a verbal assurance will not help you at a hospital counter.

This is the part most people get wrong. They assume the safety net is bigger than it actually is, right up until they need it.

Migration, Not Portability, Is Your Real Right Here

People often use the words portability and migration as if they mean the same thing and that mix-up costs them time when it matters. Portability is what you use when you already hold an individual policy and want to switch insurers at renewal. Migration is what applies to you when you are moving out of a group scheme into a retail policy and it is the right the Insurance Regulatory and Development Authority of India actually grants you at this stage.

Under the IRDAI Guidelines on Migration and Portability of Health Insurance Policies, every individual covered under a group health policy, including family members added to it, gets the option to migrate to an individual or family floater policy at the time of exit from the group. This migration carries forward the sum insured you had under the group policy along with any cumulative bonus you had built up and importantly, only the unexpired portion of your waiting period for pre-existing conditions gets applied to the new policy rather than making you start from zero.

There is a catch, though and it is one that catches people off guard.

Migration from a group policy to an individual policy is subject to underwriting. Unlike an individual-to-individual migration after four continuous years of coverage, which the insurer must accept without fresh medical scrutiny, a group-to-individual migration means the insurer can ask for health declarations, request medical tests depending on your age and sum insured and price the policy based on what they find. Corporate premiums are subsidised and spread across a large risk pool, so expect your retail premium to run higher for the same cover.

How the Numbers Actually Work Once You Migrate

|

What transfers |

How it works after migration |

Sum insured |

Carried forward up to the amount you had under the group policy |

Cumulative bonus |

Retained to the extent accrued, if any |

Waiting period for pre-existing diseases |

Only the unexpired portion applies, not a fresh 36-month wait |

Moratorium period |

Time already served counts; the current moratorium runs five years of continuous coverage |

Underwriting |

Not automatic acceptance. The insurer can ask for medical tests and price the policy based on risk |

Premium |

Usually higher than your group rate, since corporate premiums are subsidised |

Note: These are the general norms under IRDAI's migration guidelines and the 29 May 2024 Master Circular on Health Insurance Business. Actual terms depend on the specific insurer and product you migrate to, so read the policy wording before you sign.

The upside is real. You are not starting your health cover from day one the way a fresh, unrelated policy would force you to. The waiting period clock does not reset entirely and if you have already crossed a few years of continuous coverage, that history counts toward the five-year moratorium, after which insurers generally cannot reject a claim on grounds of non-disclosure barring proven fraud.

Applying for Migration Without Losing Time

Most insurers ask you to apply for migration well before your group cover actually lapses and the sooner you move, the less room there is for a coverage gap. Here is what the process usually looks like on the ground.

Step 1: Get exit confirmation from HR

You need written confirmation of your last day of group cover, along with your relieving letter or resignation acceptance, since

insurers ask for proof that you have actually exited the group.

Step 2: Approach the same insurer directly

Migration works within the same insurance company, from their group product to one of their retail products, not across insurers.

Step 3: Fill out a fresh proposal form

Since you are moving to a retail policy, you will need to declare your current health status honestly, list any ongoing treatment and

submit ID and KYC documents for every family member you want covered.

Step 4: Share your claim history if any

If you made claims under the group policy, keep discharge summaries and settlement letters ready, since the insurer will factor this

into underwriting.

Step 5: Wait for the insurer's decision

Under IRDAI norms, the insurer must communicate a decision on a migration or portability request within fifteen days of receiving a

complete application; if they do not, the request is treated as accepted.

Contact your insurer's group desk or your HR benefits team the same week you resign, not after your last day. Waiting until the policy has actually lapsed puts you in a weaker position and can mean starting the underwriting conversation from a place of urgency rather than choice.

What If Buying a Fresh Policy Makes More Sense

Migration is not the only route and for some people it is not even the better one. If you are young, healthy and were only recently added to your employer's group scheme, a brand-new individual or family floater policy bought in the open market might work out cheaper and give you more control over the sum insured, room rent limits and add-ons you actually want. The trade-off is that a fresh policy resets your waiting periods entirely, so if you or a family member has an ongoing condition, migration usually protects you better.

If you have dependents on the group cover, such as a spouse, children, or parents, a family floater bought independently can also be a sensible middle ground, particularly if the group policy's cover amount was never quite enough for your family's needs anyway.

Losing a job is stressful enough without wondering whether a hospital bill will wipe out your savings in the middle of it. SMC Insurance's advisory desk works with people through exactly this transition, comparing migration terms against fresh individual quotes so you are not choosing blind. If you want a second opinion on which route protects you better, reach out to us at SMC Insurance before your notice period runs out.

If Your Cover Came Through ESIC Instead of a Corporate Policy

Not everyone loses a company mediclaim policy when they exit a job. If your salary was within the wage ceiling for the Employees' State Insurance scheme, roughly twenty-one thousand rupees a month, your medical cover came through ESIC rather than a private group policy and the rules here are different. Full medical benefit for you and your family generally continues until the end of the contribution period tied to your last working months, not the exact day you leave. If you lost your job due to retrenchment or closure of the establishment and had at least a year of insurable employment behind you, you may also qualify for unemployment relief under the Atal Beemit Vyakti Kalyan Yojana, which comes with continued medical care for the duration you receive the allowance. Check your eligibility and remaining benefit period directly on the ESIC portal or through your regional ESIC office, since the exact cutoff depends on your specific contribution history.

Practical Steps to Avoid a Coverage Gap

A few habits make the difference between a smooth transition and a stressful one.

- Know your exact cover-end date

Do not assume it is your last working day. Confirm it in writing with HR. - Start the migration conversation early

Reach out to the insurer's group desk the week you resign, not after your notice period ends. - Keep medical records handy

Discharge summaries, prescriptions for ongoing treatment and claim history speed up underwriting. - Consider a short-term individual policy as a bridge

If you expect a gap of a few weeks before a new employer's cover kicks in, a basic individual plan can tide you over. - Check your new employer's waiting period

Many companies only add you to the group scheme after you clear probation, so ask HR when your new cover actually starts and do not let your old cover lapse before the new one begins. - Disclose everything honestly

Hiding a pre-existing condition to get a lower premium is the fastest way to get a claim rejected later.

Related reading on SMC Insurance: Health Insurance Portability and Migration Explained, Everything You Need to Know About Group Health Insurance Policy and Personal vs Group Health Insurance.

Summing Up

Your employer's health cover is tied to your job and in most cases it ends the same day you do, with no legal requirement for anyone to extend it further. What you have on your side is the right to migrate that cover to an individual or family floater policy with the same insurer, carrying forward your sum insured, bonus and unexpired waiting periods, though the insurer can still underwrite the new policy and price it accordingly. If migration does not suit your situation, buying a fresh policy in the open market or bridging the gap with a short-term plan are both reasonable alternatives. The one mistake to avoid is doing nothing and assuming you are still covered. Confirm your exact cover-end date with HR, start the migration or purchase process the same week you resign and you will walk into your next job, or your next few months of job hunting, without a gap in protection.

Disclaimer: The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product's performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents and disclosures before proceeding with any purchase or commitment.

FAQs

It typically stops on your last working day if you serve out your notice period, or immediately if your employment ends abruptly. Some employers offer a short grace period of fifteen to thirty days, but this is not mandatory and varies by company. Always get the exact cover-end date confirmed in writing from HR.

Yes, this is called migration and IRDAI guidelines give every member of a group health policy the right to migrate to an individual or family floater policy with the same insurer at the time of exit from the group. It carries forward your sum insured and any unexpired waiting period, though the insurer can still underwrite the application.

There is no single fixed number of days set out for group-exit migration under the core IRDAI guideline, so timelines can vary by insurer. In practice, apply the same week you resign to avoid any gap and always check your specific insurer's stated window before your group cover actually lapses.

No, only the unexpired portion of your pre-existing disease waiting period carries over, so you do not start from zero. If you had already served, say, eighteen months of a thirty-six month waiting period under the group policy, only the remaining eighteen months apply to the new policy.

Insurers are not permitted to charge a separate fee exclusively for migration under IRDAI norms. You will pay the premium applicable to your new individual policy based on the insurer's underwriting decision, which is usually higher than a subsidised corporate premium.

You simply have no health cover until you either migrate, buy a fresh policy, or your new employer's group scheme kicks in. Any hospitalisation during that gap would have to be paid entirely out of pocket, which is why closing this gap quickly matters.

Yes, family members who were covered under the group policy can be migrated along with you to a family floater plan, subject to the same underwriting norms that apply to the primary member.